More Americans are adding crypto to their long-term investment plans than ever before. Ownership has nearly doubled in just a few years, jumping from 15% in 2021 to 28% in 2025, but accessibility remains a big challenge, especially in retirement accounts. In 2025, an executive order was issued, allowing 401(k) retirement savings accounts to invest in digital assets.

Direct cryptocurrency ownership requires understanding wallet security, navigating complicated tax reporting, and then determining staking for certain currencies. It can be a lot, especially for those newer to cryptocurrency. Which makes understanding how to add crypto to a 401(k) crucial if you want exposure to this fast-growing asset class, without feeling overwhelmed.

That's where treasury stocks like Solana Company $HSDT make it possible to buy Solana without a wallet meaning you get exposure to Solana's price movements and can participate in this fast-growing blockchain and the broader Web3 ecosystem.

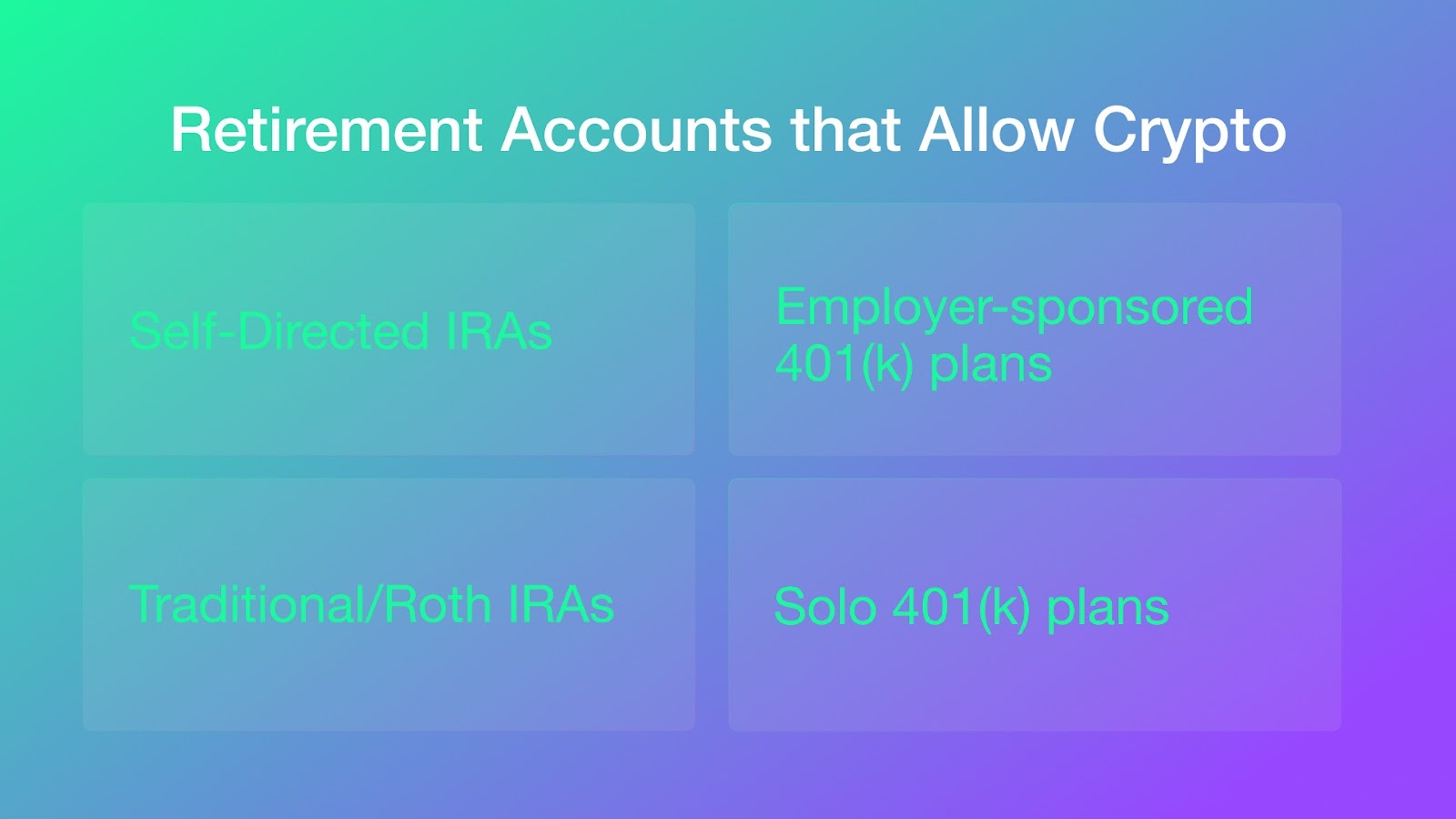

The short answer is yes, but how you do it depends on your specific retirement plan. The landscape for crypto in retirement accounts has shifted significantly, especially following regulatory changes in 2025 that rescinded previous guidance that was less favorable regarding holding digital assets in employer-sponsored plans.

One of the most accessible routes is through publicly traded stocks with crypto exposure. HSDT, the Nasdaq-listed Solana Company, operates as a digital asset treasury dedicated to acquiring and holding Solana. Created in partnership with Pantera and Summer Capital, HSDT functions as a capital markets onramp into the Solana ecosystem. Because it trades on the Nasdaq just like any other stock, you can purchase shares through most standard brokerage and retirement accounts.

This approach is part of a growing trend. Of the 142 DATCOs in existence today, 76 were founded in 2025, allowing investors to get blockchain exposure into their retirement portfolios through familiar investment channels. For those interested in Solana treasury companies or Solana treasury stocks, these publicly traded options provide a regulated path to crypto exposure.

If your employer's 401(k) plan doesn't offer crypto-related options, you still have alternatives. Opening a self-directed IRA that supports cryptocurrency investments gives you the flexibility to build the portfolio you want, including exposure to digital assets through stocks like HSDT or crypto-focused ETFs.

The type of retirement account you have plays a major role in what crypto options are available to you. Here's a breakdown of the main account types and their typical crypto access:

Adding HSDT to your retirement account sidesteps some of the headaches of direct crypto ownership: no wallets, no private keys to manage. But there are still a few things worth thinking through before you dive in.

Solana Company makes it easy to get Solana exposure if you'd rather stick with traditional financial accounts. With HSDT trading on Nasdaq, you can add Solana-linked exposure to your retirement account just as easily as buying shares of any other publicly traded company which means there's no need to worry about wallet security.

The Solana network has seen significant adoption in payments, DeFi, and tokenization, areas that may drive long-term value. Learning more about what Solana is used for can help you understand whether you want it in your retirement portfolio.

Beyond the convenience factor, there are some other reasons to consider adding crypto to your 401(k):

Solana’s focus on speed and scalability positions it well for decentralized finance and consumer applications and it's worth learning about how Solana compares to Ethereum or Solana vs Bitcoin to understand what makes each blockchain unique.

With regulatory headwinds easing and more pathways opening for crypto in retirement accounts, now may be a good time to evaluate how Solana exposure fits into your long-term strategy.

Investments in Solana, like all crypto investments, can experience significant volatility. Although there are benefits to adding crypto to retirement accounts, there is always the risk of loss, including total loss.

Yes. HSDT is a Nasdaq-listed stock, which means it can be held in virtually any retirement account that allows equity investments. There are no special legal restrictions on holding publicly traded securities like HSDT in your 401(k) or IRA, assuming your plan's investment menu includes access to individual stocks or a brokerage window.

It depends on your plan's options. If your employer's 401(k) offers a brokerage window or self-directed option, you can likely purchase HSDT shares directly. If your plan only offers a preset menu of mutual funds, HSDT may not be available. Contact your plan administrator or HR department to find out what investment options you have.

The main difference is tax treatment. In a taxable brokerage account, you'll owe capital gains taxes when you sell shares at a profit. In a traditional retirement account, gains grow tax-deferred until withdrawal. In a Roth account, qualified withdrawals are completely tax-free. For a volatile asset like crypto-exposed stocks, the tax advantages of retirement accounts can be meaningful over time.

HSDT is the stock ticker for Solana Company, a publicly traded digital asset treasury that acquires and holds Solana. When you buy HSDT stock, you're buying shares in a company whose value is tied to its Solana holdings—you're not directly owning cryptocurrency. This means you don't need a crypto wallet, don't deal with private keys, and can trade through traditional brokerage accounts during market hours.

No. Since HSDT trades on Nasdaq like any other stock, you can buy shares through your existing retirement account—no crypto wallet required. You'll use the same process you'd use to buy any other stock: search for the ticker symbol HSDT, place your order, and the shares will appear in your account.

Sources:

Crypto ownership - https://www.security.org/digital-security/cryptocurrency-annual-consumer-report/

Crypto related 401k investments - https://corpgov.law.harvard.edu/2025/06/19/trump-dol-withdraws-biden-era-esg-rule-and-crypto-guidance-for-erisa-plans/

Employer sponsored crypto 401k offerings - https://www.gao.gov/products/gao-25-106161

DATCO report - https://www.coingecko.com/research/publications/datco-report-2025

Regulatory changes expanding access to alternatives in 401k - https://www.whitehouse.gov/presidential-actions/2025/08/democratizing-access-to-alternative-assets-for-401k-investors/

This blog is for informational purposes only and does not contain all information pertinent to an investment decision. Nothing in this blog constitutes an investment recommendation or an offer of investment advisory services. This blog cannot be relied upon in making an investment decision. Nothing contained herein constitutes an offer to sell, or a solicitation to buy, any securities. This blog contains information Solana Company believes to be reliable, and has been obtained from sources believed to be reliable, but Solana Company makes no representation or warranty (express or implied) of any nature, nor accepts any responsibility or liability of any kind, with respect to the fairness, accuracy, completeness, or reasonableness of the information or opinions contained herein. Analyses and opinions contained herein (including market commentary, statements or forecasts) reflect the judgment of Solana Company as of the date this blog was published, and may contain elements of subjectivity (including certain assumptions) or be based on incomplete information.

This blog post is for informational and educational purposes only and does not contain all information pertinent to an investment decision. Solana Company is not an investment company and an investment in it does not provide the protections of the Investment Company Act of 1940. Nothing in this blog post constitutes an investment recommendation or an offer of investment advisory services. This blog post cannot be relied upon in making an investment decision. Nothing contained herein constitutes an offer to sell, or a solicitation to buy, any securities. None of the Solana Company or any of its affiliates or advisors accepts any liability for losses in connection with the acquisition, holding, or disposition of any asset, including Solana or the securities of any company. There is no assurance that following steps or other information referenced here will be effective in transacting any financial instrument. This blog post contains information believed to be reliable, and has been obtained from sources believed to be reliable, but Solana Company makes no representation or warranty (express or implied) of any nature, nor accepts any responsibility or liability of any kind, with respect to the fairness, accuracy, completeness, or reasonableness of the information or opinions contained herein. There is no guarantee that investments in any company, instrument, or type of instrument described herein will be profitable – all investments carry the inherent risk of total loss. Analyses and opinions contained herein (including market commentary, statements or forecasts) reflect the judgment of Solana Company as of the date this blog post was published, and may contain elements of subjectivity (including certain assumptions) or be based on incomplete information. There is no duty or obligation to update the contents of this blog post. This blog post is not intended to provide, and should not be relied on for accounting, legal, or tax advice, or investment recommendations. There is no guarantee that investments in any instrument or type of instrument described herein will be profitable – all investments carry the inherent risk of total loss.

© 2025 solana company. All Rights Reserved.

.svg)