Q2 2025 brought both progress and volatility for Solana. The launch of the first U.S. crypto staking ETF marked an important regulatory milestone, while network activity slowed as memecoin trading cooled. Despite the short-term pullback, these developments continue to support our long-term view on Solana’s strong competitive position and growing institutional adoption.

Late June marked a key milestone with REX-Osprey launching the first U.S. crypto staking ETF. The product gives institutional investors SOL exposure with staking yield, validating Solana as an institutional-grade blockchain and setting an important regulatory precedent.

Momentum toward a true spot Solana ETF continues to build. The U.S. Securities and Exchange Commission has asked issuers to submit updated applications by the end of July, and major firms like Fidelity have already filed.

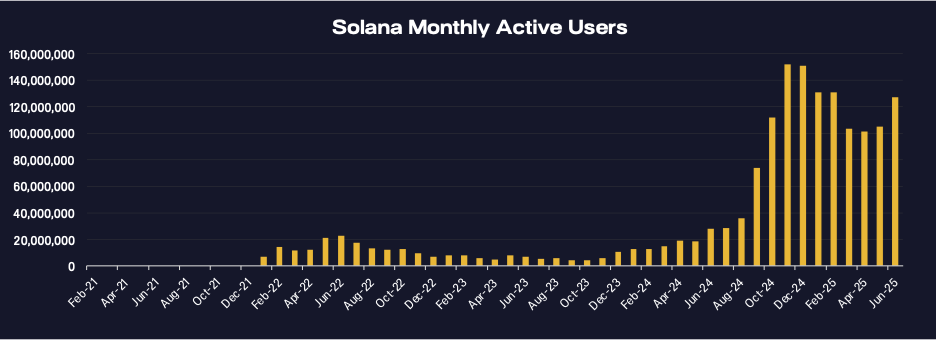

After 2024’s surge, Solana’s network activity remains strong, though below peak levels. Daily active users averaged 4–5million in Q2, down from highs above 6 million, but still represent roughly 3xyear-over-year growth and a 5–10x increase since early 2024.

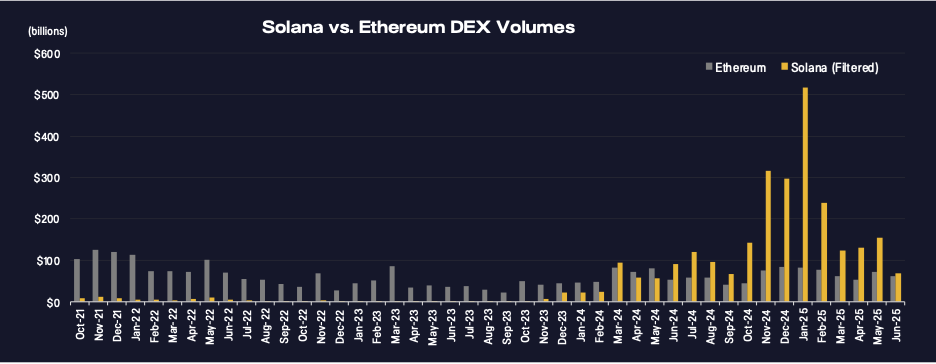

DEX volumes show a similar trend. Quarterly trading reached about $350 billion—down from Q1’speak, but still up 72% year over year—showing that Solana has built durable decentralized trading activity. Throughout the quarter, Solana remained competitive with Ethereum and continued to capture meaningful share in DeFi’s largest market.

Although the memecoin sector that drove 2024's activity has cooled, this moderation revealed durable use cases like the stablecoin market cap on Solana reaching $10 billion (4xyear-over-year growth), highlighting its utility for payments and settlements beyond trading.

Institutional adoption for Solana reached an inflection point in Q2, with major consumer platforms like MetaMask and PayPal integrating support to create seamless onramps for mainstream users.

Additionally, real-world asset tokenization gained traction as firms like R3, Superstate, and Apollo chose Solana for bringing traditional and private credit assets onto public blockchain infrastructure.

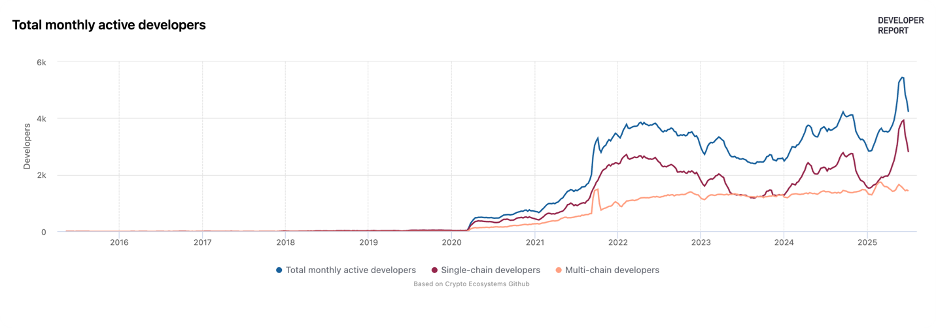

Solana remains the leading blockchain for new developers in 2025, continuing to capture most new projects across major chains due to its low costs, high throughput, and superior user experience.

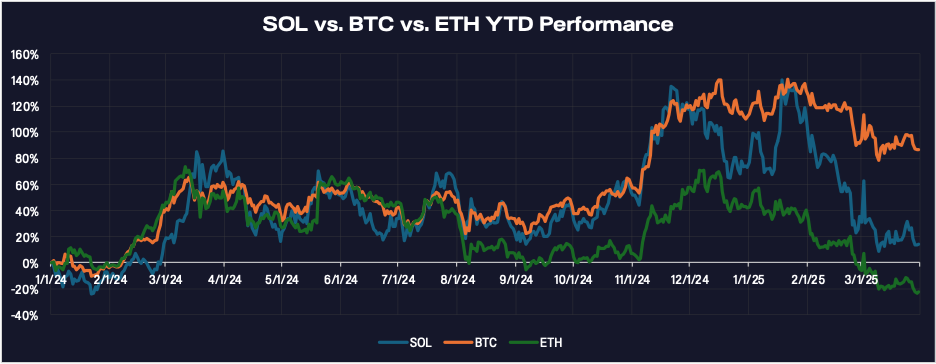

SOL traded between $130 and $180 throughout Q2, holding support despite broader market volatility. While price gains have paused, this reflects healthy consolidation after strong performance and presents attractive entry points for long-term investors.

As we enter the second half of 2025, several catalysts could drive a meaningful revaluation, including a likely spot ETF approval, continued growth in real-world asset tokenization, and ongoing technical upgrades. Together, these factors strengthen Solana’s performance edge and institutional appeal.

More broadly, Solana is evolving from an alternative blockchain into core infrastructure, increasingly competing with Ethereum for mainstream adoption. While short-term volatility may persist, the long-term fundamentals supporting Solana continue to strengthen.

This letter is for informational purposes only and does not contain all information pertinent to an investment decision. Nothing in this letter constitutes an investment recommendation or an offer of investment advisory services. This letter cannot be relied upon in making an investment decision. Nothing contained herein constitutes an offer to sell, or a solicitation to buy, any securities. This letter contains information Solana Company believes to be reliable, and has been obtained from sources believed to be reliable, but Solana Company makes no representation or warranty (express or implied) of any nature, nor accepts any responsibility or liability of any kind, with respect to the fairness, accuracy, completeness, or reasonableness of the information or opinions contained herein. Analyses and opinions contained herein (including market commentary, statements or forecasts) reflect the judgment of Solana Company as of the date this letter was published and may contain elements of subjectivity (including certain assumptions) or be based on incomplete information. Investment decisions cannot be based solely on the graphs and/or charts presented herein.

© 2025 solana company. All Rights Reserved.

.svg)